The following is an example of how a PPP loan could be received and processed by a church using IconCMO’s full-fund accounting system. Sample: PPP Loan for $100,000. For this client, all transactions will still come out of the main checking account using the General Fund and qualifying expenses will be reimbursed with the PPP… ⪼ Continue Reading…

Finance

Fund Accounting Definition – Churches & Not For Profits

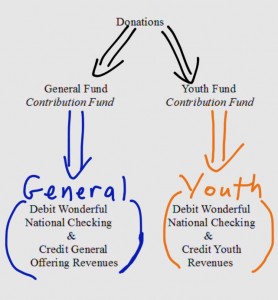

The official definition of fund accounting is described as “(1) an accounting system for recording resources whose use has been limited by the donor, grant authority, governing agency, or other individuals or organisations or by law. (2) It emphasizes accountability, rather than profitability, and is used by Nonprofit organizations and by governments. In this method,… ⪼ Continue Reading…

Church Accounting vs. For Profit Accounting

There are major differences between not-for-profit accounting and for-profit accounting. We break this down in several areas in this post. First, we’ll go over an example of for-profit accounting to get our feet wet. Next, we will move on to the not-for-profit, more specifically church accounting. In each section, we will review what questions each… ⪼ Continue Reading…

Church Accounting Software – Is It Important?

Church accounting software is important. We go over why its important, best practices, pitfalls, requirements, history, and for-profit vs not-for-profit.… ⪼ Continue Reading…

Accounting Mistakes: How to Fix Them

It’s easy to make accounting mistakes. The IconCMO fund accounting system is very flexible and has many options for correcting these mistakes. In this post, we’ll run through different types of common accounting mistakes and the best possible ways to correct them. If you’re looking for more general information on fixing errors in double entry… ⪼ Continue Reading…

Should I use Accrual Based Accounting (AP)?

This article post was originally published June 6, 2014. There are 2 types – or methods – of accounting: cash based accounting and accrual based accounting. In this post, we’ll explore the differences and the pros and cons between cash vs. accrual accounting. Cash based accounting – is when an organization writes the check out… ⪼ Continue Reading…